As job growth slows and student loan payments fully resume, consumers appear to be hanging in there. They revealed to HundredX improved perceptions of prices, likely signaling inflationary pressures continue to moderate; and Purchase Intent trends that support a stable consumer spending growth outlook.

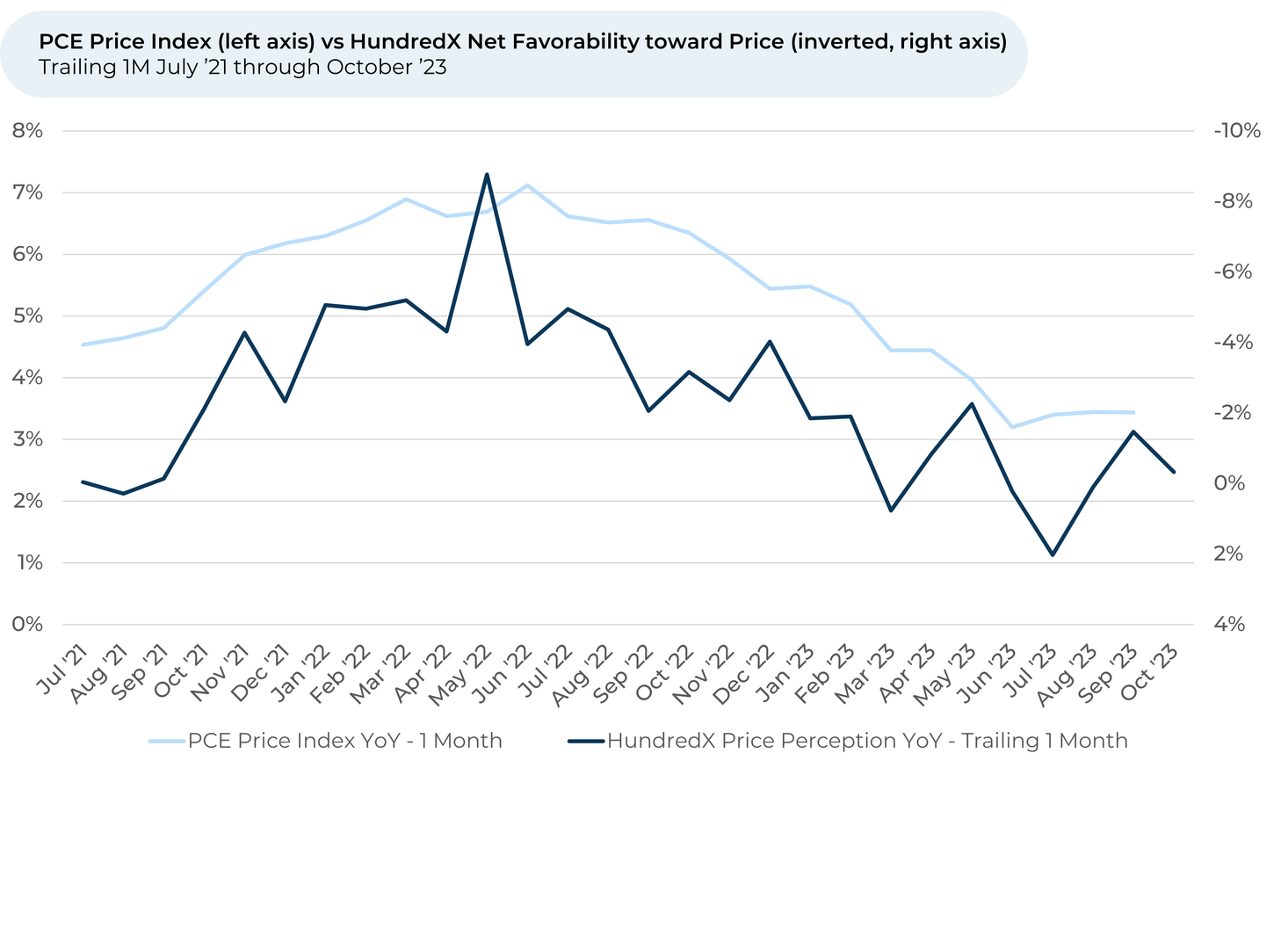

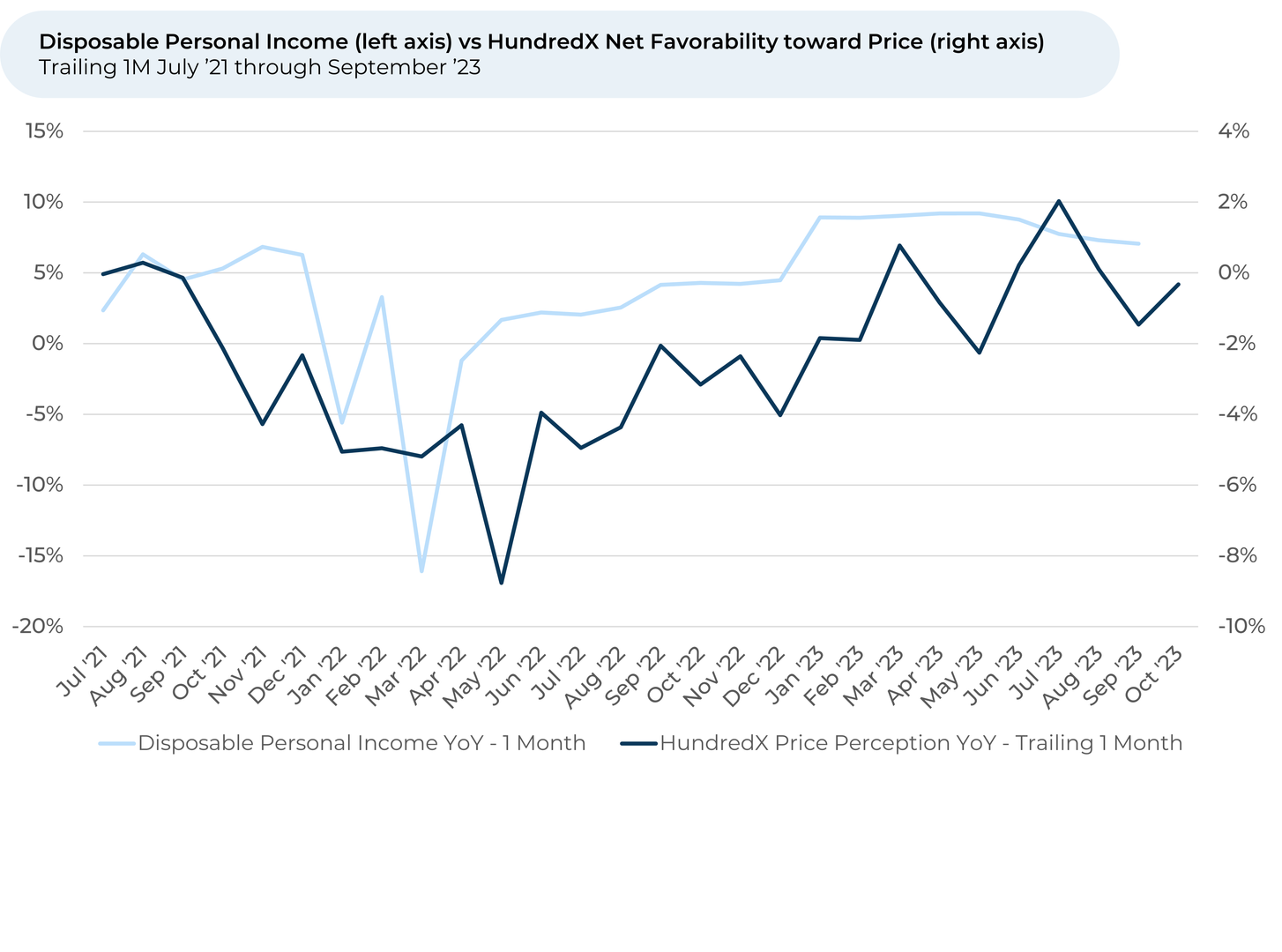

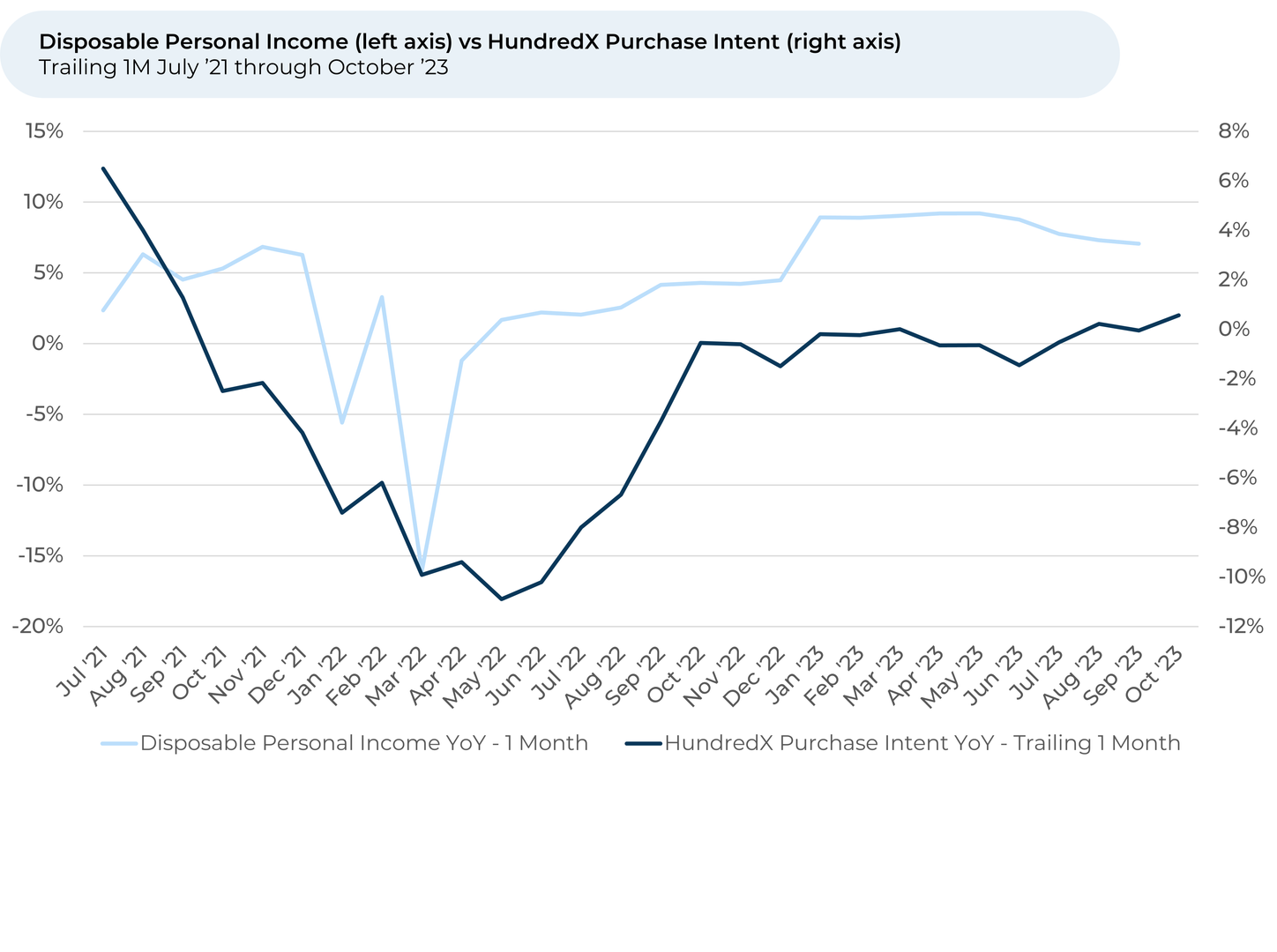

Over the past two months, customers’ overall perception of prices across all industries was up by 1%, reversing some of the 3% decline we saw over the past few months and indicating inflation may have improved last month. Changes in HundredX’s Price favorability¹,² index are typically inversely correlated with movement in the Personal Consumption Expenditures (PCE) Price levels (i.e. inflation) reported by the US government. HundredX’s Net Purchase Intent Index picked up slightly over the past few months, gaining 2% from June through October and indicating consumer spending growth outlook is picking up.

Analyzing millions of pieces of customer feedback from July 2021 across 82 industries and 3,000+ companies, we find:

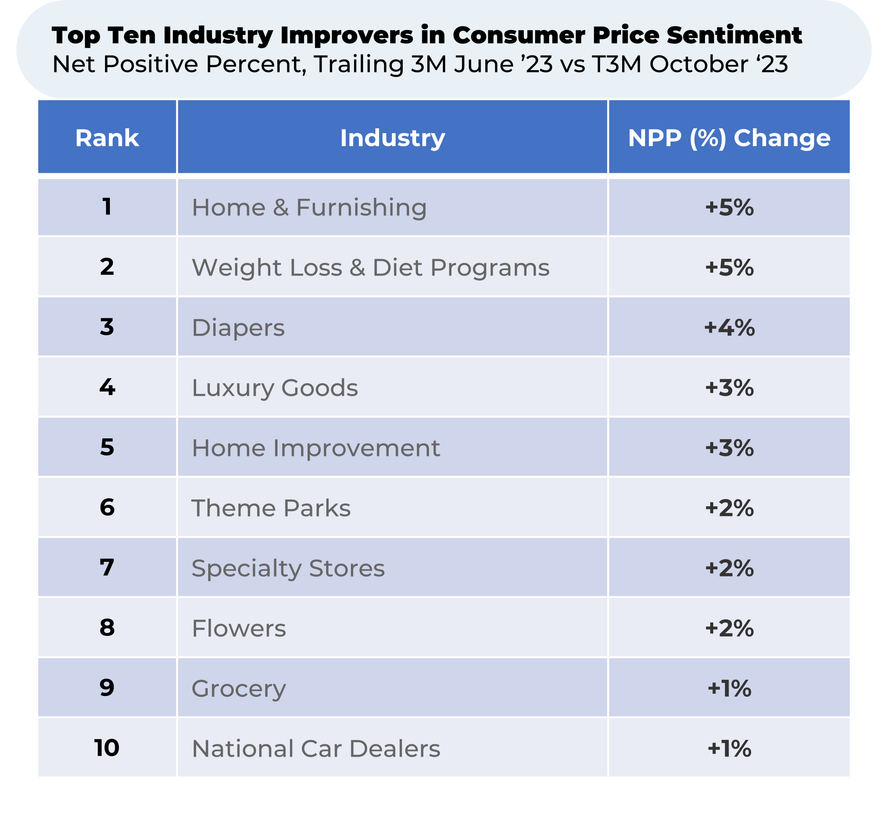

- Price sentiment and demand outlooks for weight loss and diet programs are being buoyed by increased promotions, as hype for diabetes and weight loss drugs like Wegovy, Ozempic, and Mounjaro reaches new peaks.

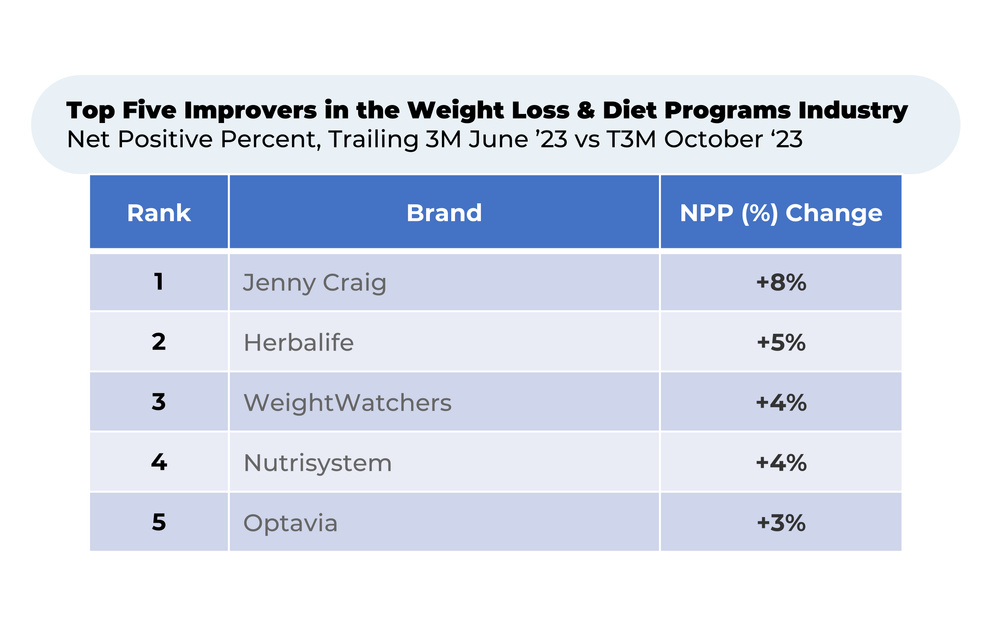

- Price sentiment for weight loss and diet programs increased by 5% over the past three months, more than all the industries we track except for home & furnishings. Usage Intent³ increased for weight loss programs during that time (+1%), likely driven by recent promotional activity as well as the industry’s push to go digital, lowering costs by slicing in-person classes and offering more digital discounts. However, customer comments indicate that, after the new or extended promotion offers expire, many customers plan to cancel, citing high prices.

- Out of the biggest weight loss and diet programs, price sentiment grew the most (+8%) for Jenny Craig over the last three months. The company officially closed in May but was recently reborn as a healthy meal-kit service after being purchased by Wellful, Inc. Customers like the price, value, and ease of use of the new model. Since Jenny Craig relaunched in September, sentiment toward value improved by 4% vs the industry and ease of use improved by 6% vs the industry. Still, it doesn’t seem quite enough to keep customers interested – Usage Intent fell 4% vs the industry as customers feel Jenny Craig’s quality has dipped.

- Customers are continuing to balk at the price of streaming services as many raise prices. Price perception toward video streaming services fell 6% over the past three month, as Apple TV Plus, Disney Plus, Hulu, Max, Netflix, Paramount Plus, and Peacock all raised prices this year. The price changes didn’t have material impacts on Usage Intent over the last three months for the group, although it fell for some services. Hulu (-2%) and Apple TV+ (-2%) declined the most compared to other top streaming services.

Please contact our team for a deeper look at HundredX's data insights into the broader economy or specific sectors, industries, or demographic groups.

- All metrics presented, including Net Purchase (Purchase Intent) and Net Positive Percent / Favorability, are presented on a trailing three-month basis unless otherwise noted.

- HundredX measures Net Favorability towards a driver of customer satisfaction as Net Positive Percent (NPP), which is the percentage of customers who view a factor as a positive (reason they liked the products, people, or experiences) minus the percentage who see the same factor as a negative.

- Usage Intent represents the percentage of customers who expect to use that brand/service over the next 12 months, minus those who intend to use less. Purchase Intent is the percentage of customers who plan to buy more from a brand minus those who intend to buy less. We find businesses that see Intent trends gain versus the industry or peers have often seen revenue growth rates, margins, and/or market share also improve versus peers.

Strategy Made Smarter

HundredX works with a variety of companies and their investors to answer some of the most important strategy questions in business:

- Where are customers "migrating"?

- What are they saying they will use more of in the next 12 months?

- What are the key drivers of their purchase decisions and financial outcomes?

Current clients see immediate benefits across multiple areas including strategy, finance, operations, pricing, investing, and marketing.

Our insights enable business leaders to define and identify specific drivers and decisions enabling them to grow their market share.

Please contact our team to learn more about which businesses across 75 industries are best positioned with customers and the decisions you can make to grow your brand’s market share.

####

HundredX is a mission-based data and insights provider. HundredX does not make investment recommendations. However, we believe in the wisdom of the crowd to inform the outlook for businesses and industries. For more info on specific drivers of customer satisfaction, other companies within 75+ other industries we cover, or if you'd like to learn more about using Data for Good, please reach out: https://hundredx.com/contact.

Share This Article